It's Sunday, your bank is closed — and 1.5 billion people don't care

It's Sunday. The branch on your corner is dark, the phone line plays hold music until Monday at nine, and somewhere a wire transfer is "processing" until Tuesday. Meanwhile, by our count, roughly 1.46 billion people woke up this morning with a bank that never noticed it was the weekend.

That number comes from doing something simple that nobody seems to do: summing every company-reported user figure across the 365 neobanks we track. Only 22 of them disclose a headline user number — so 1.46B is a floor, not an estimate. And once you chart who those users are, the story most fintech media tells falls apart.

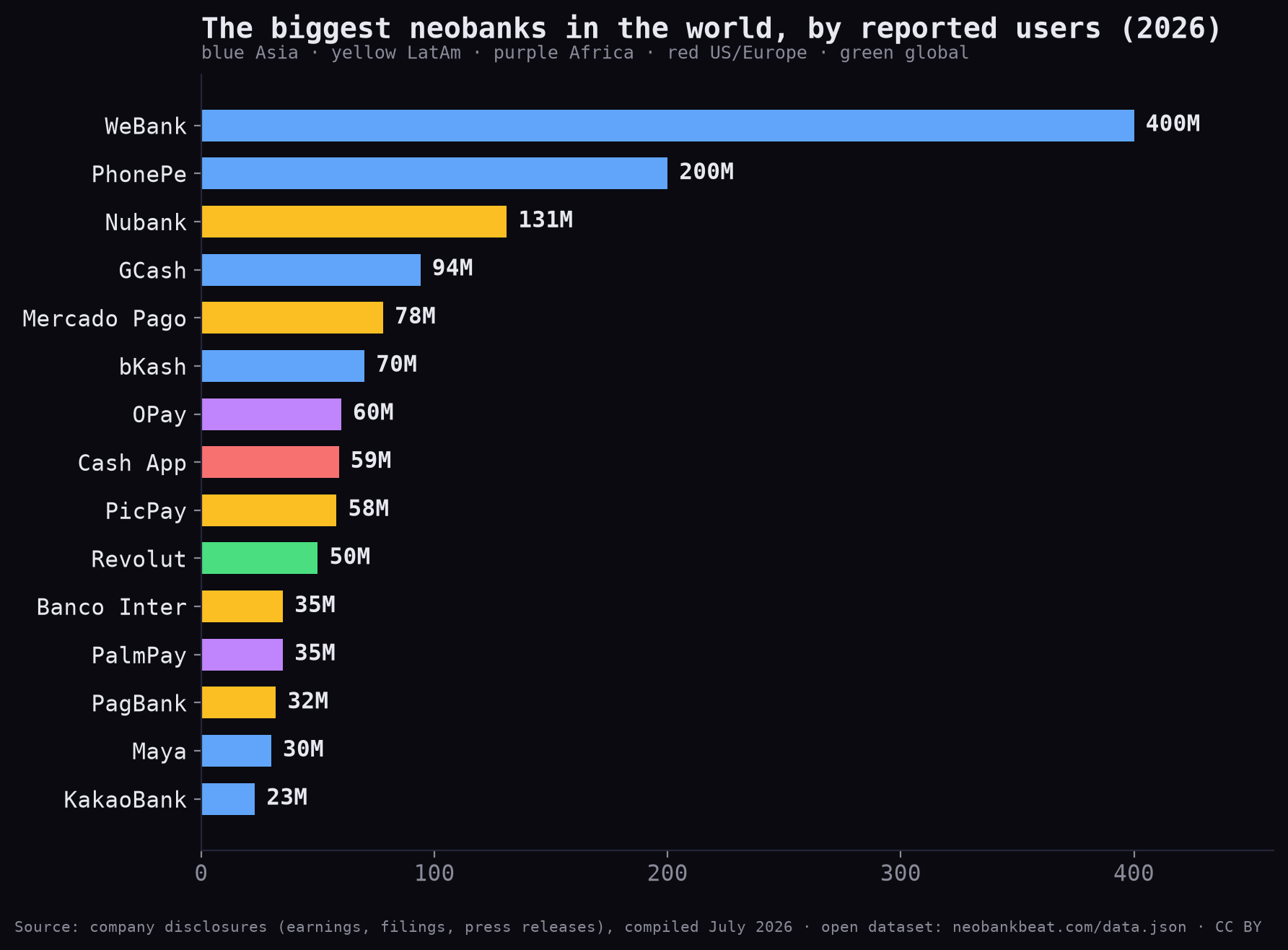

The league table isn't what the press covers

Read that top five again: WeBank (Shenzhen), PhonePe (Bengaluru), Nubank (São Paulo), GCash (Manila), Mercado Pago (Buenos Aires). The first US name is Cash App at #8. The first European one is Revolut at #10 — and Revolut is the outlier, the only Western neobank that cracked fifty million. Monzo, the UK's darling, would need to grow 33x to catch WeBank.

WeBank alone — one bank, founded 2014, profitable for years — reports more users than every US, UK, European and global-first neobank in the dataset combined, twice over.

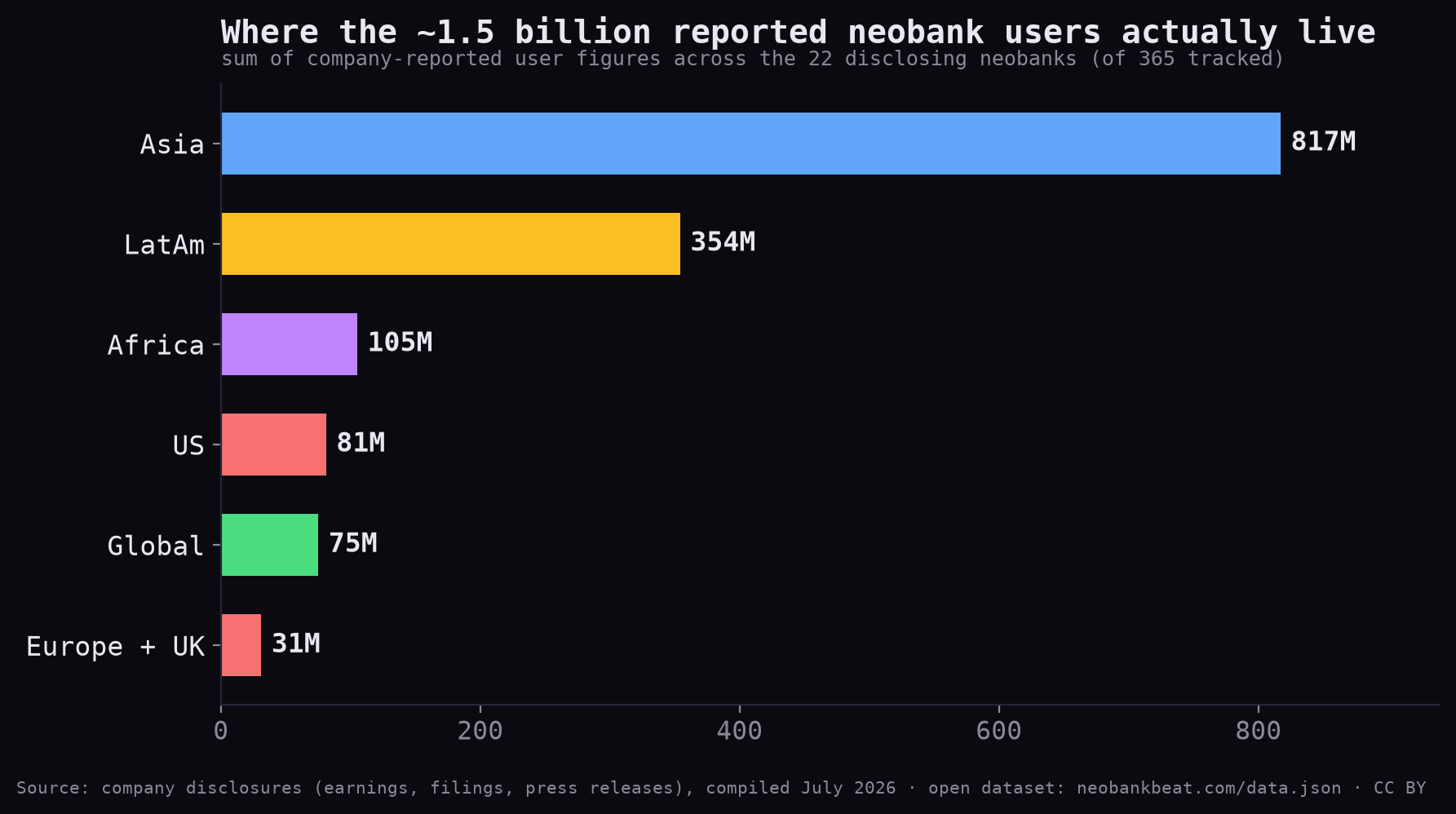

Where the users actually live

Asia holds 817 million of the reported users — 56% of everything. Latin America adds 354M. Africa, with only two disclosing entities (OPay and PalmPay, both Lagos), already outweighs the United States. Europe and the UK together: 31 million, about 2% of the total. The continent that invented the word "challenger bank" is, by user count, a rounding error.

None of this is an accident. Neobanks win hardest where the incumbent banking system failed hardest — where getting an account meant paperwork, fees and distance. That's the thesis of our underbanked deep dive: the product isn't a prettier bank, it's a first bank.

Three things the chart quietly says

1. The disclosure gap is the real story. Only 22 of 365 tracked neobanks publish a user figure. Chime went quiet for years pre-IPO; most web3-native apps report wallets or downloads, which we don't count. If the other 343 disclosed, Asia's lead would almost certainly grow — WeChat-adjacent and India-stack apps underreport, Western startups over-announce.

2. The web3 wave hasn't shown up in this metric — yet. The only self-custodial entry in the table is Phantom at 15M monthly actives. All of web3-native banking reports 25M users against traditional's 1.25B. That's either a verdict or a base camp, and after a $245M top-up week, we lean base camp.

3. Scale and safety are different axes. Being huge doesn't mean being licensed: the giants mostly hold real banking licences (WeBank, Nubank via Nu Financeira, KakaoBank), but the middle of the table is a mix of e-money wrappers and partner banks. Size is not a substitute for reading the licence line on the profile.

The Sunday point

The reason those 1.46 billion people picked these apps isn't crypto, cashback or gradient design. It's that the app works on Sunday. Instant, always-on money turned out to be a product feature the incumbent system structurally couldn't copy — branch networks and batch settlement don't do weekends. Everything else neobanks compete on is negotiable; that one thing never was.

Browse the full picture: the map view drills from region to country across all 365, every reported figure is sourced on its profile page, and the raw numbers are one click away in data.json.

User figures are company-reported and vary in metric (customers, MAU, transacting actives) — sources linked per profile; the sum is directional, not audited. Nothing here is investment advice. Spotted an error? Suggest a fix.